This guide offers key details for individuals interested in investing in brokers’ most beneficial daily liquidity CDBs, covering elements such as compensation, maturity, minimum investment amount, and liquidity.

Among the various fixed-income investments, CDBs with daily liquidity are highly favored. They are widely offered at banks and are typically the top pick for individuals looking to move away from traditional savings accounts in pursuit of higher returns.

However, if you are seeking a more appealing return, it’s important to note that brokerages also provide Certificates of Deposit (CDBs) with interest rates that are often higher than those offered by big financial institutions.

This guide has been created to provide an explanation of the functioning of the daily liquidity CDB. It includes details on various remuneration methods, maturity, minimum investment amount, and liquidity terms. By the end, you will have all the necessary information to choose the most suitable option based on your investor profile.

What does CDB stand for?

If you have previously put money into Direct Treasury, you are essentially entrusting funds to the government for management when purchasing government bonds. Likewise, when you invest in debentures, you are providing resources to a company to support their projects. The concept behind bank deposit certificates (CDBs) operates on a similar basis: individuals purchasing CDBs are effectively loaning money to banks for their credit operations.

The banks obtain funds from investors through daily liquidity Certificates of Deposit (CDB) and provide them with interest payments in return. These funds are subsequently utilized by financial institutions to provide loans to individuals.

It is important to mention that banks are required to set aside around one third of the funds they collect as a mandatory deposit with the Central Bank. This reserved amount cannot be loaned out, and this rule is in place to enable the government to regulate the volume of money in circulation within the economy.

Explanation of the process

Investing in CDBs operates on a similar principle to other fixed-income products. Explore the key aspects of this investment option.

Text: Earning potential

How much interest does a CDB with daily liquidity pay? The response varies, as there are different types of CDBs, each with unique characteristics. The three main models include:

- Text: CDB with a fixed interest rate: The investor is aware of the exact return they will earn until the investment reaches maturity, as the interest rate is determined at the time of investment. For instance, a CDB offering a 5% annual interest rate will ensure a consistent profit of 5% by the end of the investment term.

- Post-fixed CDB is the most commonly used type of CDB. Investors are aware of the indicator that will determine profitability, but the precise monetary value cannot be predetermined as it fluctuates based on the indicator’s changes. The CDI is commonly used as a benchmark, and if a CDB offers a 100% return on the CDI, the investor will receive the same return as the CDI’s performance for that year.

- Inflation-linked CDBs: The interest earned on these CDBs is a combination of a fixed rate (e.g. 5% annually) and changes in inflation, as measured by IPCA or IGP-M.

Furthermore, there is the progressive CDB, which grows in profitability as time goes on, motivating the investor to maintain their investment for a longer period.

The selection of the type of CDB depends on the investor’s characteristics and objectives. Hybrid CDBs are recommended for individuals looking to safeguard their long-term investments, while post-fixed options are better suited for those needing quick access to funds.

Smallest possible amount

Financial institutions may ask for a minimum investment amount when investing in CDBs. While big banks typically offer CDBs with lower minimum values starting at R$ 500, they come with lower returns, such as 80% of the CDI. On the other hand, brokers, who consolidate offerings from various institutions, may provide more lucrative options with higher profitability.

Paraphrased: Liquidity refers to the ease with which an asset or security can be bought or sold in the market without causing a significant impact on its price.

CDBs have different levels of liquidity. While some CDBs allow for redemption at any time, others can only be redeemed upon maturity. CDBs with daily liquidity may have blackout periods where redemption is not permitted, while those with maturity liquidity typically offer higher returns at the cost of less flexibility.

In situations where early redemption is necessary, the investor has the option to sell the CDB on the secondary market. However, the selling price may fluctuate depending on market conditions.

Expenses

Certificate of deposit (CDB) typically do not come with an administrative fee, unlike fixed income funds. While some brokers may impose brokerage or custody fees, many waive these charges. It is important to note that the overall return on investment from a CDB may differ depending on the broker, as each sets a profit margin on the paper’s value.

Here are the key factors to keep in mind when considering investing in CDBs, which offer a variety of potential returns, maturity dates, and fees, making them a compelling option within the fixed income category.

Text: Tax on earnings

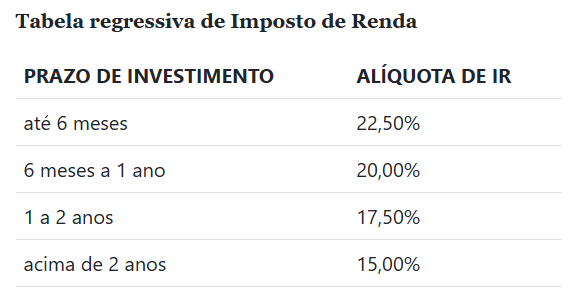

The taxation of CDBs is similar to that of other fixed-income investments. Income Tax is applied based on a regressive table, with the tax rate decreasing based on the duration of the investment. The tax rate ranges from 22.5% for investment income held for up to six months, to 15% for investments held for over two years.

Furthermore, there is a charge called the IOF (Financial Transactions Tax), which is levied only on withdrawals made within 30 days. In these instances, the rate can range from 96% to 3% of the earnings, and it decreases as the duration of the investment lengthens.

Also make sure to read:

• How to report Certificate of Deposit (CDB) in your tax return

When is something worth it? Benefits and potential dangers.

The primary concern with CDBs is credit risk, which involves the chance of the issuing financial institution experiencing financial difficulties and being unable to fulfill its obligations to investors. Thus, it is crucial to assess the institution’s reputation and financial stability before investing in a CDB.

Credit rating agencies provide valuable information as they are independent organizations that evaluate and assign ratings to companies and financial products like bonds based on their credit risk. These ratings reflect the payment ability of the institution, with higher ratings indicating a more stable and trustworthy institution, while lower ratings suggest higher risk.

Certificates of Deposit (CDBs) from institutions with greater credit risk typically provide higher returns to offset the risk. It is crucial to thoroughly assess any CDB offering a much higher profit than the market average.

How to invest in CDB? A detailed guide.

Even though CDBs are commonly recognized, it is crucial for investors to focus on specific details that can distinguish between a successful and a poor investment. To prevent any disappointments, adhere to the following five steps:

Examine the alternatives provided by both banks and brokers.

Look into the terms and conditions provided, similar to how you would when purchasing a new car. Explore the range of CDB options offered on different investment platforms. You are not required to purchase a CDB from the bank where you hold an account; instead, look for other banks that provide higher returns. Certain brokers, like XP, offer CDB options from multiple banks, simplifying the comparison process.

Select the Certificate of Deposit (CDB).

Please respond to these four inquiries for every Certificate of Deposit (CD) you are evaluating.

– What level of profitability is being provided?

Can you clarify what you mean by “maturity”?

– Can you explain what the liquidity system is?

– What is the level of risk associated with the issuer?

By having this information, it will be simpler to select the most suitable option based on your objectives. If you require access to the funds prior to your salary, you may want to consider a CDB with daily liquidity. For those looking for a CDB with higher credit risk, it might be beneficial to explore options that provide increased profitability. Additionally, it’s important to monitor the variance in profitability among different brokers.

Create an account

When selecting a CDB, create an account with the broker. The procedure is typically straightforward, involving providing personal details and submitting documents like ID and tax ID. Apart from the available CDB options, review the redemption timeframe and user-friendliness of the platform. Additionally, consider exploring other investment products offered by the broker if you intend to diversify your investments.

Keep an eye on the restrictions set by the FGC.

The maximum coverage limit is R $ 250,000 per individual and per institution. To enhance protection, it is advisable to spread investments across multiple banks. Nevertheless, starting from 2017, the FGC has implemented an overall limit of R $1 million guaranteed every four years.

Send money and begin investing.

To begin, you can transfer your existing account funds to the broker, typically within a day, using DOC or TED. Once the deposit is made, you can proceed to purchase the selected CDBs. Wishing you successful investments!

Could you please provide the specific text that you would like me to paraphrase from the Infomoney article “What is CDB?”

Comments